Society

Too Fast, Too Furious: Việt Nam's War on Flat-Rate Taxes

Minh Viễn wrote this Vietnamese article, published in Luật Khoa Magazine on June 20, 2025. A new government policy is

Minh Viễn wrote this Vietnamese article, published in Luật Khoa Magazine on June 20, 2025. A new government policy is

Thiên Lương wrote this Vietnamese article, published in Luật Khoa Magazine on June 18, 2025. A proposal from VinSpeed and

Key Events * Việt Nam Abolishes Death Penalty for Corruption Amid Wave of High-Profile Trials * Chinese Survey Ship Operates Near Việt

Your donations to charitable foundations or sponsored non-profit organizations (NPOs), like CHANGE, are also subject to taxation in Vietnam.

Thuy Tung wrote this article in Vietnamese, which was published in Luat Khoa Magazine on October 4, 2023. Lee Nguyen translated the article into English.

According to the regulations, charitable, humanitarian, and educational promotion contributions shall be deducted from the taxable income of businesses, salaries, and wages before calculating your personal income tax incurred by a resident taxpayer in Vietnam. [1] [2] These contributions include:

The documentation proving charitable, humanitarian, and educational promotion donations are receipts issued by central or provincial-level organizations and funds.

The personal income tax deduction rate for these contributions ranges from 0 to 35%, depending on the annual income of each donor to the mentioned funds.

Recent examples of donations for charitable funds include the calls to support the Fund For the Poor or the COVID-19 Vaccine Fund. [7] [8] Recently, there was an appeal to support the victims of a fire in a mini apartment building, which was implemented by the agency system of the Hanoi Municipal Vietnam Fatherland Front Committee. [9]

Annually, the heads of sub-quarters or village chiefs, on behalf of the commune-level Vietnam Fatherland Front Committee, must visit each household to collect donations for disaster relief funds, study promotion funds, poverty reduction funds, etc.

All these humanitarian contributions are subject to personal income tax.

The issue is that the law does not allow anyone to deduct these donations from their taxable income if there is a lack of receipts. Without proper proof of these contributions, these funds will not be deductible when calculating personal income tax.

Citizens often question the transparency when using the above-mentioned humanitarian funds. However, they often overlook the need for receipts for their charitable and humanitarian contributions to these funds to qualify for personal income tax deductions.

During donation campaigns, there is also a lack of information from the Vietnam Fatherland Front Committee or relevant authorities about providing receipts donors can use for personal income tax deductions.

A good example of this would be the case when the Hanoi Municipal Vietnam Fatherland Front Committee for the Fund For the Poor started a call for public donations in 2023. [10] Apart from information about the bank account numbers for the government to receive money, there is no mention of the personal income tax exemption procedures for these contributions and no receipts for the donors. This call is captured in the screenshots right below.

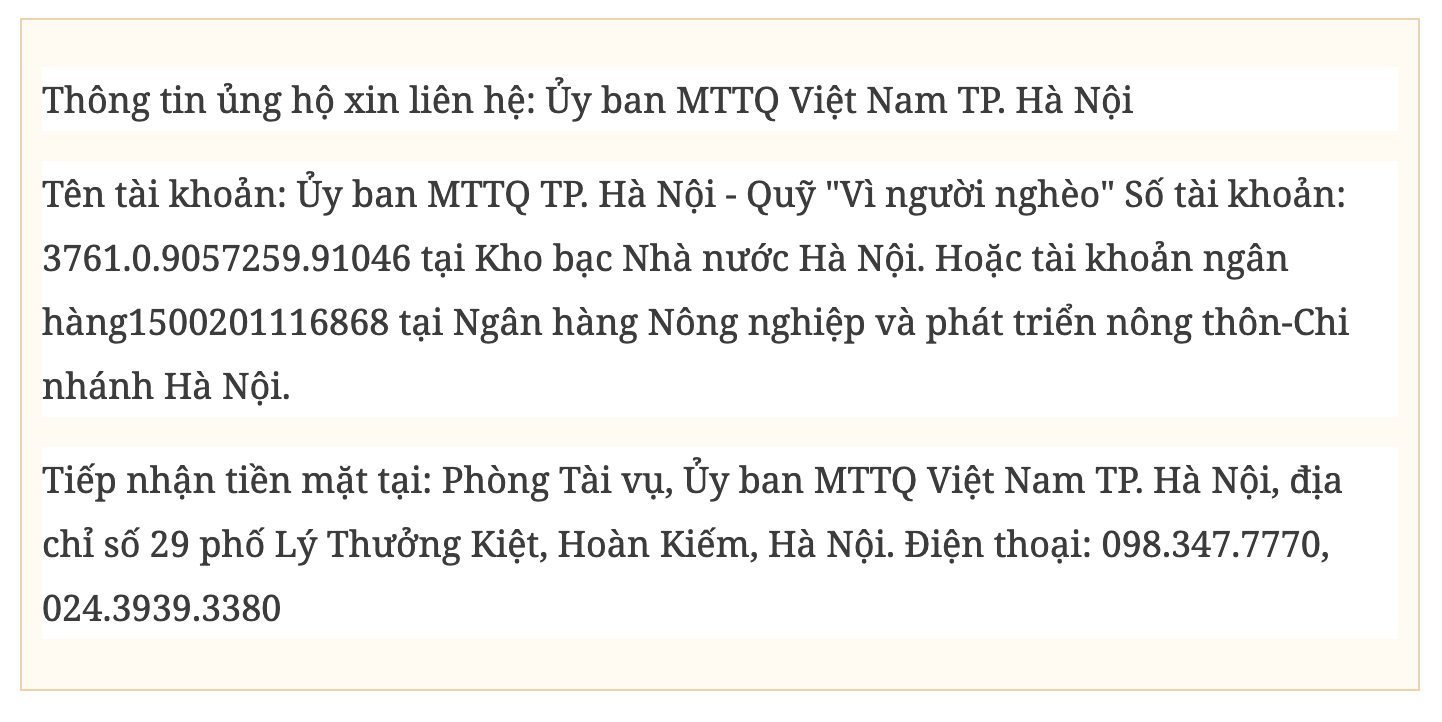

Translation:

For support information, please contact the Hanoi Municipal Vietnam Fatherland Front Committee

Account name: the Hanoi Municipal Vietnam Fatherland Front Committee - the Fund “For the Poor”; Account number: 3761.0.9057259.91046 at Hanoi State Treasury. Or bank account number 1500201116868 at The Vietnam Bank for Agriculture and Rural Development - Hanoi Branch.

Receive cash at the Finance Department, the Hanoi Municipal Vietnam Fatherland Front Committee, address No. 29 Ly Thuong Kiet Street, Hoan Kiem District, Hanoi City. Phone number: 098.347.7770, 024.3939.3380

If the donations are not deducted, the citizen donors may have to pay anywhere from 0 to 35% personal income tax on every donation they contribute to these funds. That's right, Vietnamese citizens have to pay personal income tax on their donations!

The tax rate may be higher or lower depending on the annual income of each individual, along with various deductions and progressive tax brackets from 1 to 7. Bracket 1 has a tax rate of 0%, followed by 5%, 10%, 15%, 20%, 25%, 30%, and the highest at 35% in bracket 7.

The establishment decisions and operating permits of scientific and technological organizations allow the NPOs to receive financial support from individuals within and outside the country to carry out community activities.

CHANGE is one such organization. The investigation against Hoang Thi Minh Hong also confirmed this fact. [11] [12]

Since Vietnamese law narrows the scope of charitable and humanitarian activities, scientific and technological organizations are not among the mentioned funds or organizations.

In this context, individuals are considered purchasers of services or goods from scientific and technological organizations when donating to the organizations' community activities. Therefore, they cannot use receipts from these organizations for personal income tax deductions.

In this situation, sponsors must also pay value-added tax, potentially even corporate income tax, and personal income tax, on each donation.

First, the state will impose a 5% or 10% output VAT on scientific and technological organizations, depending on whether they register for tax directly or use the deduction method, as mentioned in previous articles.

If registered using the deduction method, individual sponsorship amounts will be deducted from the input VAT of goods and services purchased by the organizations for their activities. If profits arise from these sponsorships, the Vietnamese state will impose a 20% CIT.

In CHANGE's case, as it did not register for tax using either method, the state imposed a 5% VAT and a 5% CIT, totaling 10%, on individual sponsorship amounts for CHANGE.

If scientific and technological organizations do not issue output VAT invoices, donations are treated as income of the organizations. Consequently, the Vietnamese state will impose a 20% CIT on each sponsorship amount. [13]

From this, it is evident that each donation made for the community activities of scientific and technological organizations will be subject to taxes ranging from a minimum of 5% to a maximum of 55% according to the above tax calculation formulas. These include personal income tax, VAT, and/or CIT.

1. Clause 3, Article 9, Circular No. 111/2013/TT-BTC on the Implementation of the Law on Personal Income Tax, the Law on the Amendments to the Law on Personal Income Tax, and the Government's Decree No. 65/2013/ND-CP Elaborating several Articles of the Law on Personal Income Tax and the Law on the Amendments to the Law on Personal Income Tax (n.d.). Thư Viện Pháp Luật. https://thuvienphapluat.vn/van-ban/Thue-Phi-Le-Phi/Thong-tu-111-2013-TT-BTC-Huong-dan-Luat-thue-thu-nhap-ca-nhan-va-Nghi-dinh-65-2013-ND-CP-205356.aspx?anchor=dieu_9

2. A resident individual is an individual who is present in Vietnam for 183 days or more in a calendar year or 12 consecutive months, counting from the first date of their presence in Vietnam, in which the arrival date and departure date are calculated as a day.

3. Decree No. 68/2008/ND-CP Prescribing Conditions and Procedures for the Setting up, Organization, Operation, and Dissolution of Social Relief Establishments. (n.d.). Thư Viện Pháp Luật. https://thuvienphapluat.vn/van-ban/Giao-duc/Nghi-dinh-68-2008-ND-CP-dieu-kien-thu-tuc-thanh-lap-to-chuc-hoat-dong-giai-the-co-so-bao-tro-xa-hoi-66552.aspx

4. Decree No. 81/2012/ND-CP Amending and Supplementing several Articles of the Government’s Decree No.68/2008/ND-CP of May 30, 2008. (n.d.) Thư Viện Pháp Luật. https://thuvienphapluat.vn/van-ban/lao-dong-tien-luong/nghi-dinh-81-2012-nd-cp-sua-doi-nghi-dinh-68-2008-nd-cp-quy-dinh-dieu-kien-149164.aspx

5. Decree No. 30/2012/ND-CP on the Organization and Operation of Social Funds and Charity Funds. (n.d.). Thư Viện Pháp Luật. https://thuvienphapluat.vn/van-ban/Van-hoa-Xa-hoi/Nghi-dinh-30-2012-ND-CP-to-chuc-hoat-dong-quy-xa-hoi-tu-thien-137920.aspx

6. Decree No. 93/2019/ND-CP Prescribing Organization and Operation of Social and Charity Funds (latest update). (n.d.). Thư Viện Pháp Luật. https://thuvienphapluat.vn/van-ban/Tai-chinh-nha-nuoc/Nghi-dinh-93-2019-ND-CP-ve-to-chuc-hoat-dong-cua-quy-xa-hoi-quy-tu-thien-398154.aspx

7. Hà Nội: Kêu gọi ủng hộ Quỹ ‘Vì người nghèo’ năm 2023. (2023, September 30). thanglong.chinhphu.vn. https://thanglong.chinhphu.vn/ha-noi-keu-goi-ung-ho-quy-vi-nguoi-ngheo-nam-2023-103230907163423896.htm

8. Bộ Y tế. (2021, September 1). Thủ tướng: Quỹ vắc xin COVID-19 là quỹ của sự nhân ái, tinh thần đoàn kết và trái tim kết nối trái tim. Bộ Y Tế. https://covid19.gov.vn/thu-tuong-quy-vac-xin-covid-19-la-quy-cua-su-nhan-ai-tinh-than-doan-ket-va-trai-tim-ket-noi-trai-tim-1717355873.htm

9. Chung tay ủng hộ các nạn nhân trong vụ cháy chung cư mini. (2023, September 18). thanglong.chinhphu.vn. https://thanglong.chinhphu.vn/chung-tay-ung-ho-cac-nan-nhan-trong-vu-chay-chung-cu-mini-103230918161642.htm

10. See [7]

11. Investigation conclusion No. 554-25, dated August 24, 2023, of the Police Investigation Agency under the Ho Chi Minh City Public Security Department.

12. Indictment No. 467/CT-VKS-P3, dated August 30, 2023, of the Ho Chi Minh City People's Procuracy.

13. Decree No. 218/2013/ND-CP Detailing and Guiding the Implementation of Law on Corporate Income Tax. (n.d.). Thư Viện Pháp Luật. https://thuvienphapluat.vn/van-ban/Doanh-nghiep/Nghi-dinh-218-2013-ND-CP-huong-dan-thi-hanh-Luat-thue-thu-nhap-doanh-nghiep-217811.aspx

Minh Viễn wrote this Vietnamese article, published in Luật Khoa Magazine on June 20, 2025. A new government policy is

Key Events * Việt Nam Abolishes Death Penalty for Corruption Amid Wave of High-Profile Trials * Chinese Survey Ship Operates Near Việt

The Human Rights Measurement Initiative (HRMI), a global collaborative project involving human rights practitioners and academics, has released its 2025

Anh Băng wrote this Vietnamese article, published in Luật Khoa Magazine on June 20, 2025. The Vietnamese government has just

Vietnam's independent news and analyses, right in your inbox.